Luxury isn’t what it used to be: What’s happening to the world’s most exclusive brands?

Lower consumption in China, the trade war, and an oversaturated market are taking a toll on the sector, which has lost 50 million customers in one year

For the first time in a long time, the luxury sector is experiencing a period of uncertainty. After the boom of recent decades and the significant growth peak it experienced during the pandemic, it is now going through what some experts describe as a period of stabilization, others as a period of regression, or even, the most pessimistic, as a burst bubble. The decline in consumption in China, the main engine of growth, has weighed down the world’s leading brands, led by France and Italy. Economic uncertainty, now exacerbated by Donald Trump’s tariff war, is another factor, while inflation and rising prices have further shaken demand.

Due to the combination of all these factors, 50 million consumers have vanished in the last two years, according to the annual luxury study by the consulting firm Bain Company and the Italian Altagamma, one of the leading European associations in the sector. The luxury clientele numbered 350 million in 2024, down from 400 million in 2022. Spending reached €1.5 trillion ($1.7 trillion) in 2024, a slight decline of 1%. These are the worst figures since the 2008 financial crisis. A few weeks ago, the firms revised their 2025 forecasts downward, anticipating a sales decline between 2% and 5%.

“The industry has developed significantly over the past 40 years, and we’re now in a phase of uncertainty and stabilization, which has been amplified by the difficulties in China and now also in the U.S. Fifty years ago, this was a small industry targeting a few consumers, but it has become massive, and today it’s a global industry with groups present in every market,” explains Delphine Dion, professor at Essec Business School.

Personal luxury goods (fashion, leather goods, jewelry), which are the core of the sector, experienced their first contraction in 15 years, with spending declining by 2% in 2024 to €363 billion ($412 billion), mainly due to a drop in demand from Generation Z (those born after 1997), who are more price-sensitive. Ultra-wealthy clients account for 40% of the revenue of major brands, further reinforcing the sector’s polarization.

“More than a slowdown, we are seeing a return to the pre-COVID period. The pandemic was an exceptional moment, and we are now returning to normal, but it is true that inflation is rising, which has affected demand for affordable luxury,” says luxury historian Sabine Pasdelou. Although growth has been slower these pase two years, if we take 2019, before COVID, as a reference, the industry has grown 15% to date.

The sector is currently facing its own contradictions: by definition, it is exclusive, but it has become more accessible. In this process, part of the excellence that defines it — rooted in its artisanal nature (the savoir-faire) — has been lost. It used to be for a select few; now it’s for many. Once timeless, luxury now follows trends. If luxury used to be ordinary for extraordinary people, now it is the extraordinary of the ordinary.

“In these booming years, luxury has become blurred, it has turned into accessible luxury, built through marketing to reach the middle class. Access has become democratized, and there’s a fashion component; when its essence was timelessness, you bought something for life, or you inherited it,” explains Stephano Venchiarutti, a consultant at the Gentils Pariziens agency, who believes that “this bubble, fueled for so many years, is beginning to deflate.”

“We are witnessing a regression: before, the priority was savoir-faire; now everything is industrial, and we have entered a kind of madness where the luxury label is slapped on, but people want to buy status, not craftsmanship, but logos,” says Abraham de Amézaga, an industry expert and professor at ISG Luxury Management.

Between 2019 and 2023, unprecedented demand for luxury goods allowed the sector to grow by 5%, according to McKinsey Company. Price increases accounted for more than 80% of growth during this period. For Ignacio Marcos, senior partner at the consultancy firm, “it’s true there are factors slowing down growth, such as lower Chinese demand, but there are areas that complement this consumption, like the U.S., which is growing, as well as Japan, with India as one of the emerging markets.”

Uneven impact

Only a third of brands worldwide recorded business growth in 2004, compared to 95% in 2021 and 65% in 2023, according to Bain & Company. The impact is uneven: some categories, like personal luxury goods, which are more accessible to price-sensitive average consumers, have been more affected, while others are more resilient, maintaining the values of exclusivity and inaccessibility and targeting the ultra-rich, who are less affected by uncertainty.

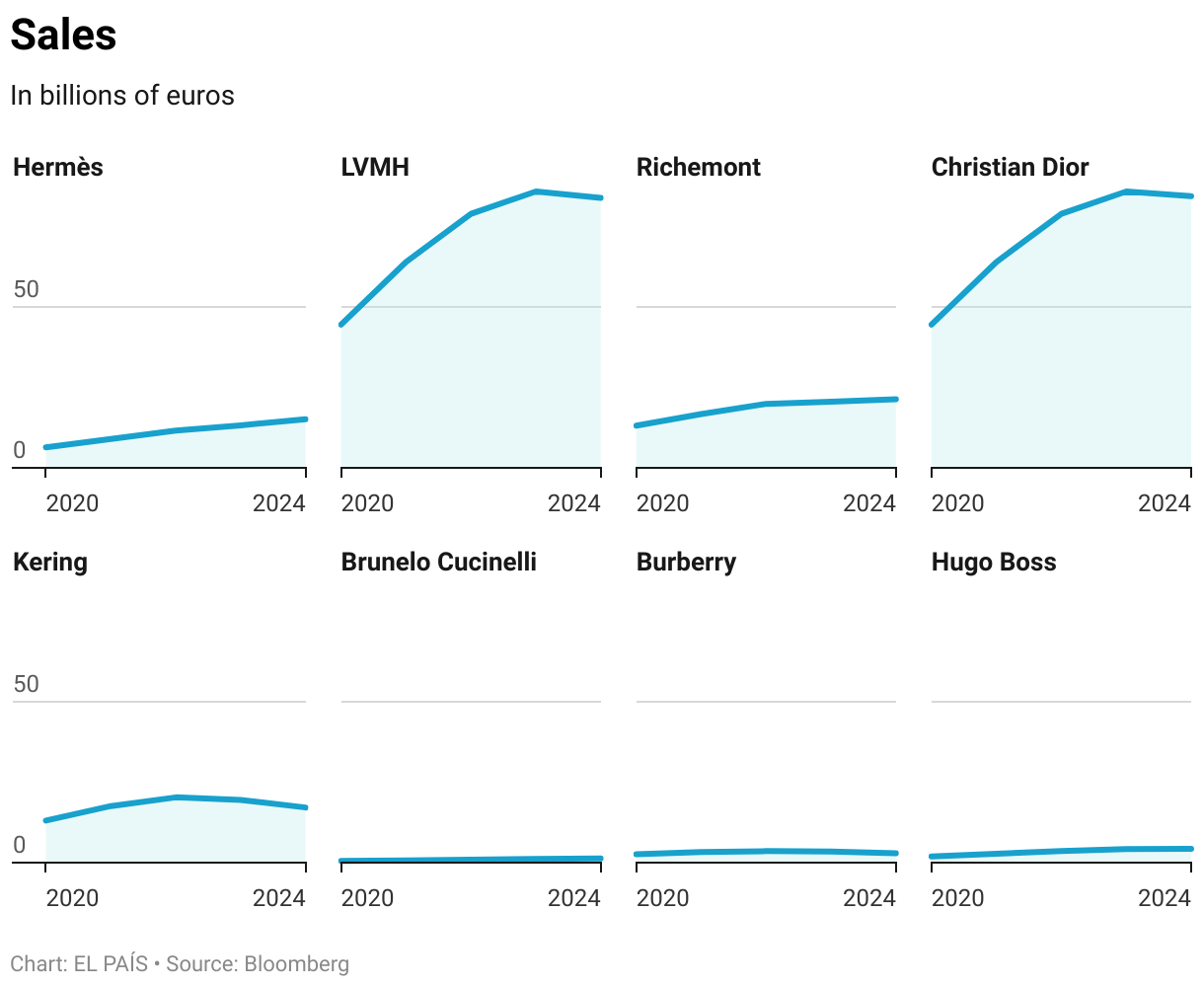

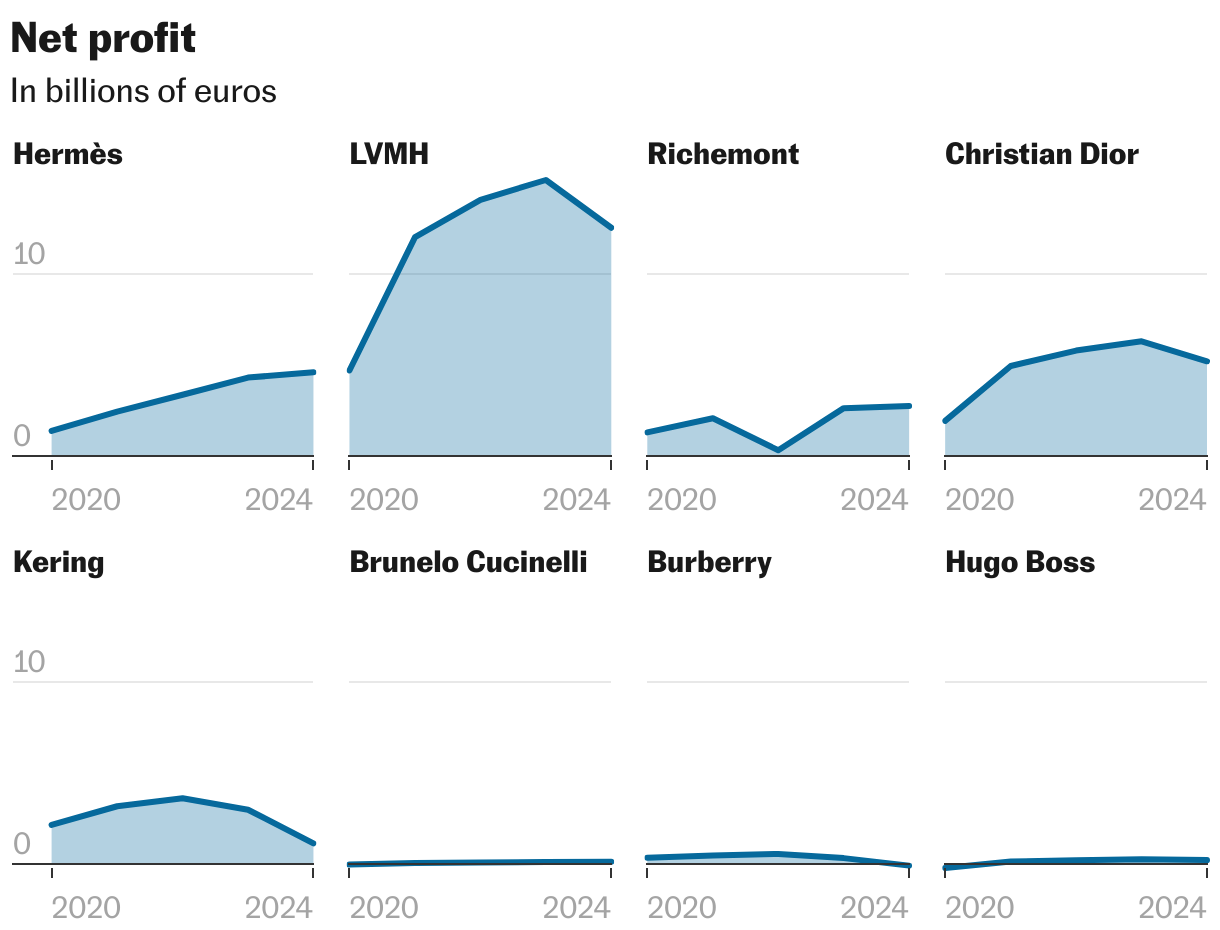

The world’s largest luxury giant, LVMH — an empire built by the Frenchman Bernard Arnault in the 1980s and now encompassing 90 brands including Christian Dior and Louis Vuitton — saw its revenue drop by 2% in 2024, hurt by declining Chinese demand, which accounts for 25% of its global sales. The second-largest group, Kering (Gucci, Saint Laurent), founded by French billionaire François Pinault, fared worse. Its revenue fell 12%, dragged down by its flagship brand, Italian fashion house Gucci.

Only a few companies have been able to weather the downturn. This is the case of the Swiss group Richemond, owner of the Cartier watch brand, which increased its sales by 10% in the last quarter. Meanwhile, the Prada group, which recently acquired Versace from the U.S. multinational Capri Holdings (Michael Kors), grew by 17%, and the French company Hermès grew by 15%.

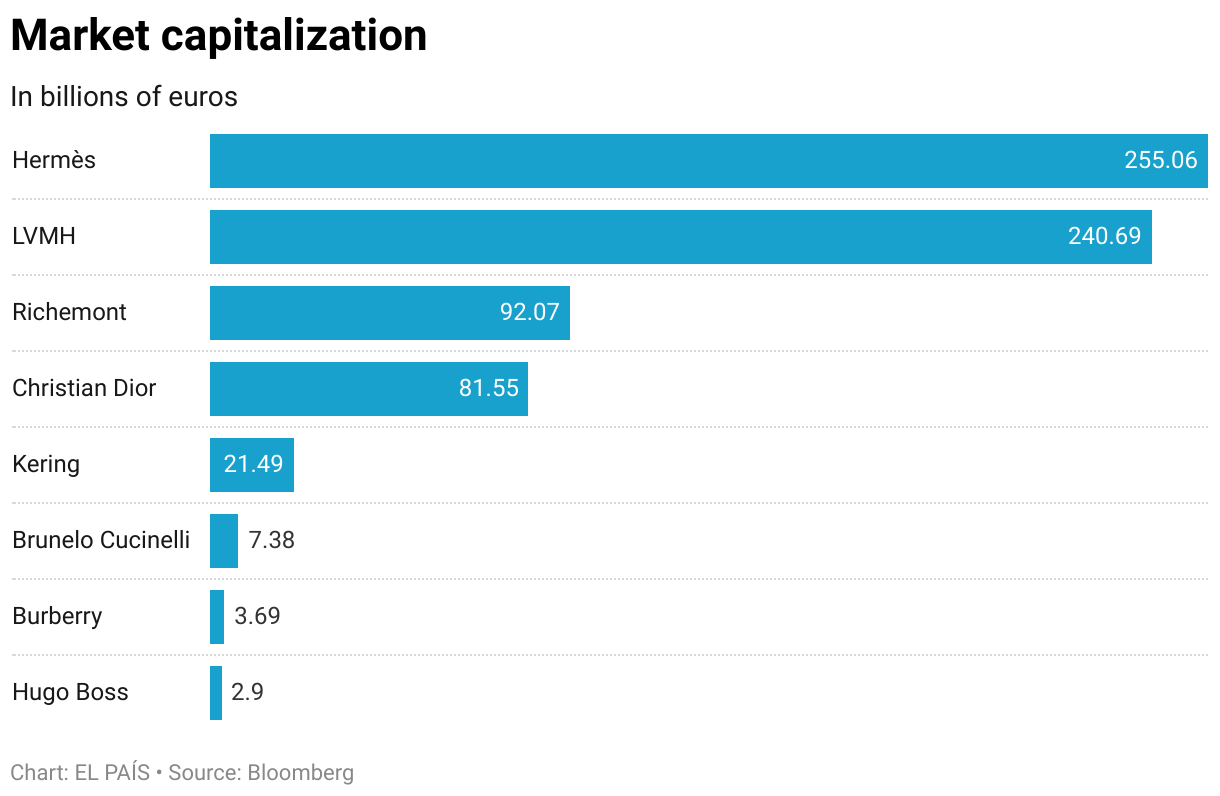

In a scenario of stock market declines for most companies, Hermès hit a milestone a few weeks ago when it surpassed the giant LVMH in market capitalization for the first time in history, becoming the leader of the CAC 40, the main index of the Paris Stock Exchange, and the third most valuable stock in Europe by market value. This is one of the case studies highlighted by experts because, as Venchiarutti points out, “their strategy has always been the same — they have respected the value of savoir-faire.”

In this expansion process, “groups have had to adapt their product portfolios to different customer segments, and some brands have shifted toward so-called silent luxury, as opposed to brand-name luxury. Those that have adapted best to these changes are more resilient today,” explains Ignacio Marcos.

Gucci and Hermès — polar opposites in a slowing market — exemplify these two strategies. “Gucci’s customers no longer buy into the quality-price ratio, which they consider excessive, while Hermès customers do see added value. Gucci has become mass-market, whereas Hermès remains an object of desire. They have taken opposite paths,” says Ukrainian designer Fedor Savchenko, an expert in the sector and owner of the Desmalter brand.

By category, jewelry and watches have fared better, as they are still considered investments. Some watch brands (certain Rolex models) have waiting lists that last years, much like Hermès with its Birkin bags. A similar situation occurs with the car manufacturer Ferrari.

“For these brands, luxury remains about access. They may not sell you the most exclusive first product, but they will sell you the second, which earns you points to access the first. To get on list A, you have to have gone through list B,” explains Ignacio Marcos. This makes them a safe haven asset during periods of crisis or instability.

The Chinese slowdown

The fall in Chinese demand, one of the triggers of the current crisis, is related not only to the country’s economic situation, but also to a change in consumer behavior. The younger generation (aged 25 to 35) now represents 40% of luxury customers and one-third of luxury sales.

“There’s one factor to consider: China is developing its own luxury product; it wants to take its place in the sector and demonstrate that Made in China is equivalent to French savoir-faire. The government has invested heavily in the fight against counterfeiting and has attracted talent, people who have studied or worked for brands in Europe and who understand this savoir-faire and are applying it locally,” says Pasdelou, who believes that “we must end this Western, Franco-Italian vision of luxury. China is demonstrating its capacity to produce quality high-end products. It’s an essential focus today.”

In fact, aside from Prada’s recent purchase of Versace, recent acquisitions have been made by groups from Beijing or Qatar. In 2018, the Chinese group Icicle acquired the French brand Carven, and two years earlier, Mayhoola, which is owned by the Qatari royal family, took over Balmain. In 2012, a Qatari fund wrested Valentino from the British firm Permira.

Experts rule out major mergers but do believe there may be acquisitions focused on so-called “sleeping beauties” — “those small luxury houses with heritage that have an expert clientele who aren’t looking for status, and who have a stamp of identity and storytelling,” says Pastelou.

One of today’s challenges is to attract — or win back — a more elusive customer, who is less loyal than before, more demanding, and questions value for money more than ever.

“We’ve seen brutal price increases in recent years. A bag that cost €1,800 [$2,050] before COVID now costs €2,500 [$2,840]. Today, people are wondering if it’s worth what they’re paying,” says Amézaga. At the same time, “the problem is that quality has dropped, while prices are rising for no apparent reason,” Venchiarutti points out.

Experts agree that, in the process of adapting production to meet rising demand, brands have lost some of their artisanal value. This has led to a sort of demystification of certain products in some fashion houses, “which no longer meet any of the three criteria: exclusivity, quality, or timelessness,” Marcos points out.

The outsourcing of production has also devalued part of the prestige, as the notion of something being “made at home” is lost. Added to this is the double-edged sword of social media, which serves as a showcase but also as a public complaint box for dissatisfied consumers. On platforms like TikTok, many customers have posted videos denouncing the poor quality of purchased products.

“There’s a kind of luxury fatigue due to this overexposure on social media, which has generated a feeling of excess and exhaustion. Social media has a lot of power, and an influencer can be an incredible way to gain customers, or on the contrary, it can cause a major crisis, precisely because trust no longer resides in the brand, but in its influencers,” says Venchiarutti, who warns that these tools “have somewhat trivialized the sector.”

Second-hand boom

Price hikes have triggered a boom in the second-hand luxury market, offering buyers slightly lower prices or access to items unavailable in stores. A Hermès Birkin bag, which has years-long waiting lists, sells for even more on resale platforms — especially collectible editions.

“This will continue. Especially in accessories, watches, and jewelry, there will be an upswing because they allow accessibility and because secondary markets offer more reasonable prices,” says Marcos.

Another trend, driven by shifting consumer motivations, is the move from material to experiential luxury. In 2024, spending in this category rose by 5%. Increasingly, customers prefer — rather than owning a $15,000 handbag — to sleep in a hyper-exclusive castle, dine at a three-Michelin-starred restaurant with a years-long waitlist, attend a one-of-a-kind fashion show, or even travel to space.

According to Carlos Sánchez, senior partner at McKinsey, “the exceptional nature of luxury today is now sought in experiences, which already account for more than half of luxury consumption in Spain.”

Luxury brands have been investing in this shift for years. Groups like LVMH and Kering have diversified into high-end hospitality and even the art world. Cartier hosted a VIP masquerade ball in a Venetian palace, and in 2022, Saint Laurent flew its most elite clients to a runway show in the Sahara Desert.

“Since the pandemic, we’ve placed more value on exceptional moments than on material things, no matter how exclusive they may be. Consumers have evolved in this sense and are more interested in spiritual luxury and less in possessions,” explains Pasdelou.

Despite current uncertainty, the market is expected to rebound and reach €2.5 trillion ($2.8 trillion) by 2030, with annual growth projected between 5% and 9%, according to McKinsey forecasts.

“This is a very resilient industry; there are solid foundations for growth, aand the number of ultra-wealthy individuals continues to rise each year,” says Marcos.

Sustainability

For luxury brands, the key challenges are capturing this emerging demand, “finding new ideas, maintaining exclusivity for VIP clients, and at the same time, being able to secure mass-market business, which accounts for half of brands’ revenue,” says Pasdelou.

Other challenges, according to the expert, include: “Building loyalty among veterans, winning back lost customers, and attracting emerging customers. Also, sustainability — creating luxury that doesn’t have an impact. It’s about figuring out how to continue growing and innovating, while meeting these ethical requirements, in a society that’s evolving at a dizzying pace.”

Bain & Company highlights the potential of emerging markets to attract and compensate for the decline in Asian — or potentially North American— demand. Regions like Latin America, the Middle East, India, and Africa could add over 50 million upper-middle-class luxury consumers by 2030 — the very ones lost over the past two years.

The trade war launched by U.S. President Donald Trump has created a new source of instability, although experts downplay its significance. They believe it is too early to assess the impact and argue that the market will continue to grow. Some groups, such as Hermès and LVMH, have already announced that they will pass the cost of these tariffs on to their price tags.

Carlos Sánchez of McKinsey also points out that tariffs “can create a disruption in the supply chain, but their real impact on price will not be as great, as the tariff would not be applied to the final cost. A 30% tariff on a €10,000 [$11,400] handbag does not mean that a €3,000 [$3,400] price increase will be applied.”

The year 2025 marks a crossroads for the luxury industry — a pivotal moment, analysts agree, for the sector to hit reset and emerge from its existential crisis.

“Groups need to rethink their strategy and reposition themselves,” says Dion. “It’s an opportunity to reclaim the core of what luxury truly means, to reconsider the mass-market expansion, and to return to its essence. That doesn’t mean going backward, but it does mean accepting that future growth rates will likely be more moderate than in the past — though we mustn’t forget that the ultra-wealthy, those who can spend €50,000 [$57,000] a year on luxury, will always be around,” the expert concludes.

The complex succession of family clans

French businessman François-Henri Pinault recounts that back in 2003 his father invited him to dinner and told him he wanted to retire.

“The dinner took place on a Thursday. When I walked into our headquarters the following Monday, I found entirely new furniture in my office — and my father sitting at the desk. ‘You don’t work here anymore— you work there,’ he said, pointing to the corner office that had been his," Pinault recalled in an article in the Harvard Business Review.

That’s how François Pinault, 88, handed him the reins of the Kering group, which he founded in the 1960s and today is the world’s second-largest luxury conglomerate.

Securing the succession process to preserve the legacy of these family businesses is one of the major headaches for luxury magnates, many of whom are elderly and, in most cases, aim to put their heirs in charge. In the Italian brand Prada, founded in 1913, Miuccia Prada (76 years old) has placed her son, the racing driver Lorenzo Bertelli, within the group, although it is unclear whether he will take the reins.

Donatella Versace is 65 years old and has been leading the Italian company since 1997. She could leave it in the hands of her daughter, Allegra, the majority heir. Giorgio Armani founded his brand in 1975. Last year on his 90th birthday, Armani — who has no children — said he would stay at the helm for a couple more years. Although he has always defended the brand’s independence, he did not rule out selling it as part of his succession plan. “I think the best solution would be a pool of trusted people close to me and chosen by me,” he said.

Bernard Arnault, owner of the world’s largest luxury group LVMH (Louis Vuitton, Christian Dior), is 76 years old and has been preparing his succession for decades, although for now he is not handing over control and will continue leading for another 10 years, until he is 86. The age limit for leadership at the publicly traded company was 80, but shareholders voted at the group’s last general meeting to change the rules. The change was supported by 99.18%.

Arnault, the richest man in France, has five children. All are involved in the company. Four of them sit on the board or hold strategic positions within the group. According to Aline Pozzo di Borgo, luxury consultant at ISC School, the billionaire “has positioned his children, each in their own sector, although Delphine, the eldest, is the one who could take the reins,” she says.

Delphine Arnault, 50, is in charge of Christian Dior, which along with Vuitton, is one of the pillars of LVMH. The Arnault family owns 48% of the group’s capital and 64% of the voting rights. “Succession in this particular case is a major issue, as it’s unlikely there will be another big-name empire like this,” says the expert.

They all want to avoid inheritance battles like the one Gucci experienced after the murder of Maurizio Gucci in 1995. “People talk about the children, but we mustn’t forget that these businessmen are not alone; they have a trusted team around them, although in most cases they intend to stay until the end,” says Sabine Pasdelou, a luxury sector historian.

At Hermès, the heirs of the founder Émile-Maurice Hermès and main shareholders created a company to protect themselves against LVMH, which was quietly increasing its stake in the brand and reached 20%. Over the past two decades, the global giant has acquired dozens of Italian brands like Fendi and Bulgari, while its rival Kering took over Gucci. Pasdelou points out that, besides ensuring corporate governance, “there is a question of preserving genetic heritage; it’s about forming alliances to preserve high society, that kind of oligarchy.”

Sign up for our weekly newsletter to get more English-language news coverage from EL PAÍS USA Edition