Germany’s paralysis threatens European economy

Analysts and institutions expect flat growth in 2024 and fear that the country’s stagnation may spread to France and Italy

Europe’s economic engine remains stalled. And just as when Germany sneezes the eurozone catches a cold, the main EU capitals are closely watching everything that is happening in Berlin. At the moment, the outlook is not at all promising. The country’s five large economic research and analysis institutes have sharply lowered their forecasts for 2024: if just half a year ago, the German economy was expected to grow 1.3%, now the forecast has been cut to just 0.1%.

These revisions are taking place after German gross domestic product (GDP) fell by 0.3% in 2023, leading German Economy Minister Robert Habeck to describe the outlook as “dramatically bad.” The coming months — with the first interest rate cuts in sight — will be key to determining whether the country manages to get out of the hole it has found itself in.

Tractors shutting down Berlin as farmers protest. Deserted airports in Frankfurt and Hamburg. Bleak train stations in Munich. These are just some of the images that have been captured in Germany in the last three months. The country is simultaneously dealing with union demands for workers to regain their purchasing power and an economy brought to a standstill. This situation is beginning to affect the rest of Europe. And for good reason: Germany still represents more than a quarter of the wealth of the eurozone. “The eurozone economy is growing less due to the strong dependence and interconnection between Germany and other countries such as France and Italy,” explains Raymond Torres, director of Economics at the Savings Banks Foundation (Funcas). “It is still early to know what will happen in the medium term, but in the short term the impact is clearly negative.”

The main international institutions — such as the International Monetary Fund (IMF) and the Organization for Economic Co-operation and Development (OECD) — have already warned about a possible contagion effect. All projections point out the timid progress of countries such as France and Italy and, consequently, of the eurozone itself. At the end of January, the IMF forecast for 2024 predicted growth of 1% and 0.7% for Paris and Rome, respectively, with the eurozone forecast to grow by 0.9%. A few days later, the OECD followed suit, forecasting growth of 0.6%, 0.7% and 0.6%.

The two organizations, however, put the forecast for Spain — for now less exposed to Germany — at 1.5%. “Spain is in better shape than the rest of the EU,” the European Commissioner for Economy, Paolo Gentiloni, stated in an interview with EL PAÍS. And although countries like Spain are pushing the economy further, their momentum is not enough to compensate for Germany’s stagnation.

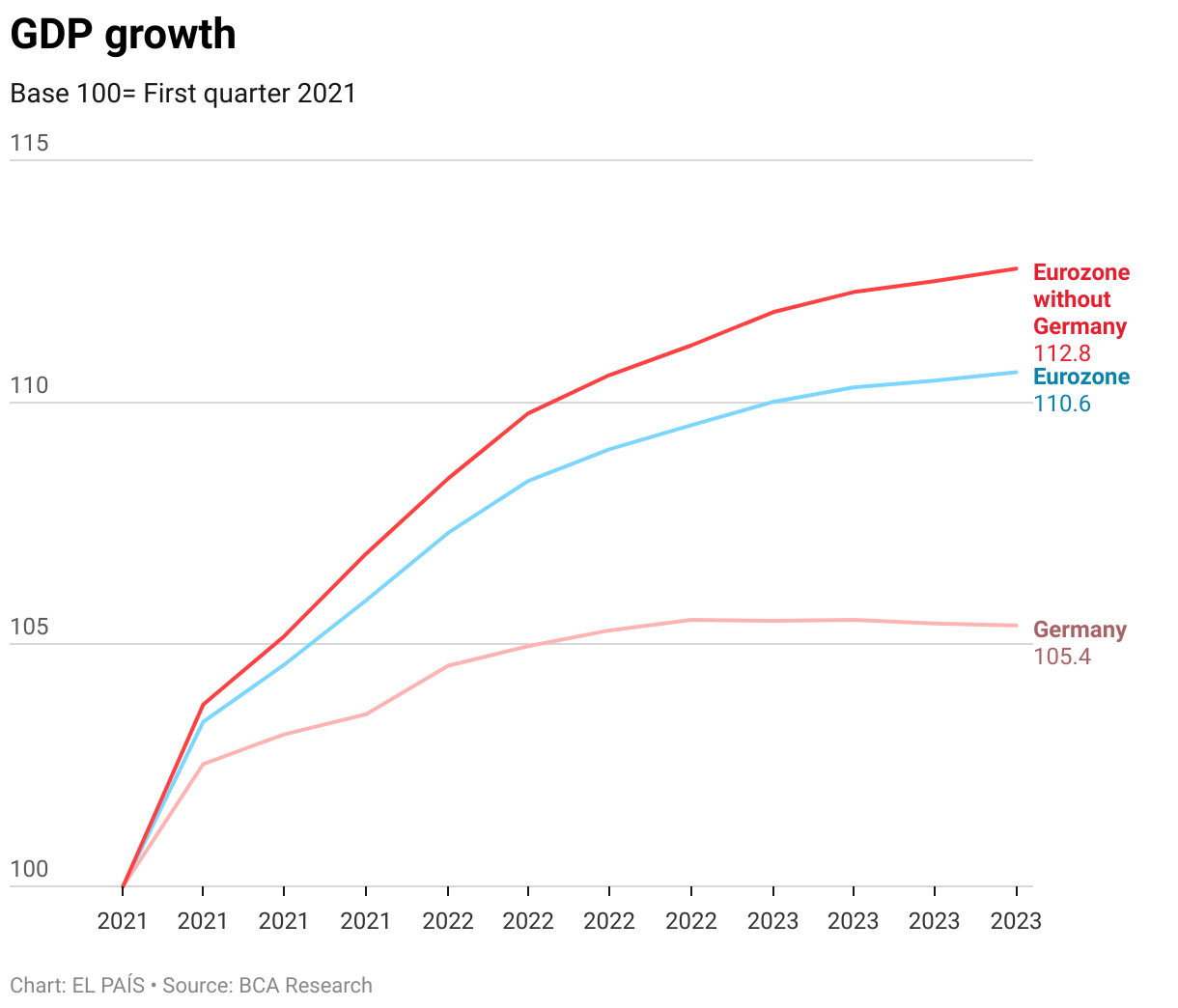

Indeed, analysts at the consulting firm BCA Research believe that the eurozone could enter a slight recession in 2024, even if the entire European Union manages to avoid it. After all, Germany still accounts for 28% of the euro area economy. In the recently published The Rest Of Europe Versus Germany, BCA Research concludes that, if it were not for Germany, the eurozone’s GDP would have grown by 12.8% in the last three years, compared to 10.6%, the official figure. The problem, according to BCA’s head of European strategy, Mathieu Savary, is that this trend will continue as long as Berlin continues to face material obstacles such as those related to the energy transition, fiscal austerity measures, real estate problems and weak external demand. “These headwinds are depressing consumption and, therefore, the national GDP.” All these difficulties, he adds, are having significantly less effect in other EU countries.

In the case of Germany, Torres continues, the country is facing the combined effect of two economic shocks. One is related to inflation, the sharp rise in rates and families’ loss of purchasing power, which affects private consumption. This situation has also affected other European markets, but its impact has moderated over time. The second shock, says Torres, is intrinsic to the German nation and is linked to the change in its productive model, meaning the consequences are structural in nature.

Until a few years ago, the German national economy was buoyed by the cheap supply of Russian energy and by outsourcing part of its production to Asian countries, mainly China. In other words, it is more dependent on Moscow and Beijing than other EU countries, which has sweeping consequences given the current geopolitical tensions and the push to transition to green energy. The country’s decision to stop buying Russian gas after the start of the war in Ukraine had obvious consequences. But it is also important to look at China, Germany’s second-largest non-EU trade partner. The drop in exports to China and the increased competition in the automobile sector, particular in electric vehicles, has taken a heavy toll.

Another factor is the weak investment activity of companies in Germany. In the short term, says Timo Wollmershäuser, economic analyst and deputy director of the Ifo Institute, German industry is suffering from weak global demand for capital and intermediate goods, i.e. precisely those in which German industry specializes.

In addition to weak exports, there is “the great uncertainty regarding the economic policy of the German government,” says Wollmershäuser. And this has prompted companies to postpone their investment decisions. For this reason, he says, “Germany has become less attractive as a business location.” According to Wollmershäuser, other reasons include high taxes, bureaucratic obstacles, slow-moving digitalization, high energy prices and labor shortages. Due to all these factors, the IMF estimates that Germany will be the G7 country with the slowest growth in 2024: last year, it was the only economy in the group to contract.

Opportunity for the south

BCA Research believes that slowed growth in Germany may pull down the eurozone or have a contagion effect on other economies, such as France or Italy. The global growth momentum of the last 12 months appears to have largely bypassed Europe. The region has been grappling with the aftermath of high energy prices, high interest rates to control inflation, and weak consumer confidence. “These headwinds have especially affected manufacturing companies, including those in Germany,” says Alfred Kammer, IMF European Director.

According to analysts, the divergence between Germany and the rest of Europe — particularly in the south — will increase this year, as the former continues to stagnate and the latter improves. According to the European Commission, Spain is expected to grow 1.7% in 2024 and 2% in 2025, while Greece, Portugal, Malta, and Cyprus are also forecast to see strong gains.

But Ángel Talavera, head of the European economics department at Oxford Economics, believes the south will not be able to lift the entire region: “Inevitably, Germany’s stagnation will lead the eurozone to another year of very low growth,” he explains. Berlin, like the rest of the EU, is affected by the interest rate rises. But Talavera insists the country is facing additional problems such as low demand — especially external — and regulatory hurdles with long waiting times for project approval, which is an obstacle for investment.

Torres says that given the difficulties in Germany, many multinationals may reconsider where they invest and set up office. For now, this is not leading to relocations, however, “trend changes are beginning to be seen in terms of new investments,” he says.

The IMF argues that, even if growth were to bounce back in the short term, the growth prospects for Europe will remain timid unless there is reform. Alfred Kammer points out that per capita income in Europe is a third lower than the average in the United States, and also says it is important for the region to improve productivity and realize the potential of the single market by “reducing internal barriers.” This must be complemented by changes at the national level, he adds: in Germany, “there is significant scope to reduce bureaucracy and barriers to new business creation.”

Sign up for our weekly newsletter to get more English-language news coverage from EL PAÍS USA Edition