Germany is staring at the end of its economic model

The war in Ukraine and its repercussions, compounded by structural problems such as an ageing population and a lack of investment, spell the end of the boom

Ever since Russian Tsar Nicholas I coined the phrase “the sick man of Europe” in the mid-19th century, this has been a term that has changed hands like a boxing belt over the years. Originally used to indicate the decline of the Ottoman Empire, it has evolved into the favorite description of a great economy in decline. While in recent years the United Kingdom has had the dubious honor of holding the title, the war in Ukraine and its aftermath have brought a new candidate to the fore: Germany. The world’s fourth largest economy and Europe’s biggest is in turbulent waters and is confronting structural problems that could spell the end of almost two decades of prosperity for the Old Continent’s economic powerhouse. According to the International Monetary Fund (IMF), it will be the only developed economy that does not experience growth this year.

You have to go back to the early 2000s to find the last time when Germany challenged for the title, when its economy was deflating — with GDP falling in two consecutive years in 2002 and 2003 — and struggling with poor external demand and double-digit unemployment rates. Gerhard Schröder, chancellor from 1998 to 2005, initiated a series of reforms that triggered a jobwunder (employment boom) and, combined with healthy foreign demand from booming economies such as China, boosted the German economy’s backbone. This comprises a competitive manufacturing sector, largely thanks to cheap Russian gas and Eastern European labor. These factors have propped up Germany for almost two decades, making it Europe’s leading force. However, some experts warn that its success may have caused Berlin to become complacent.

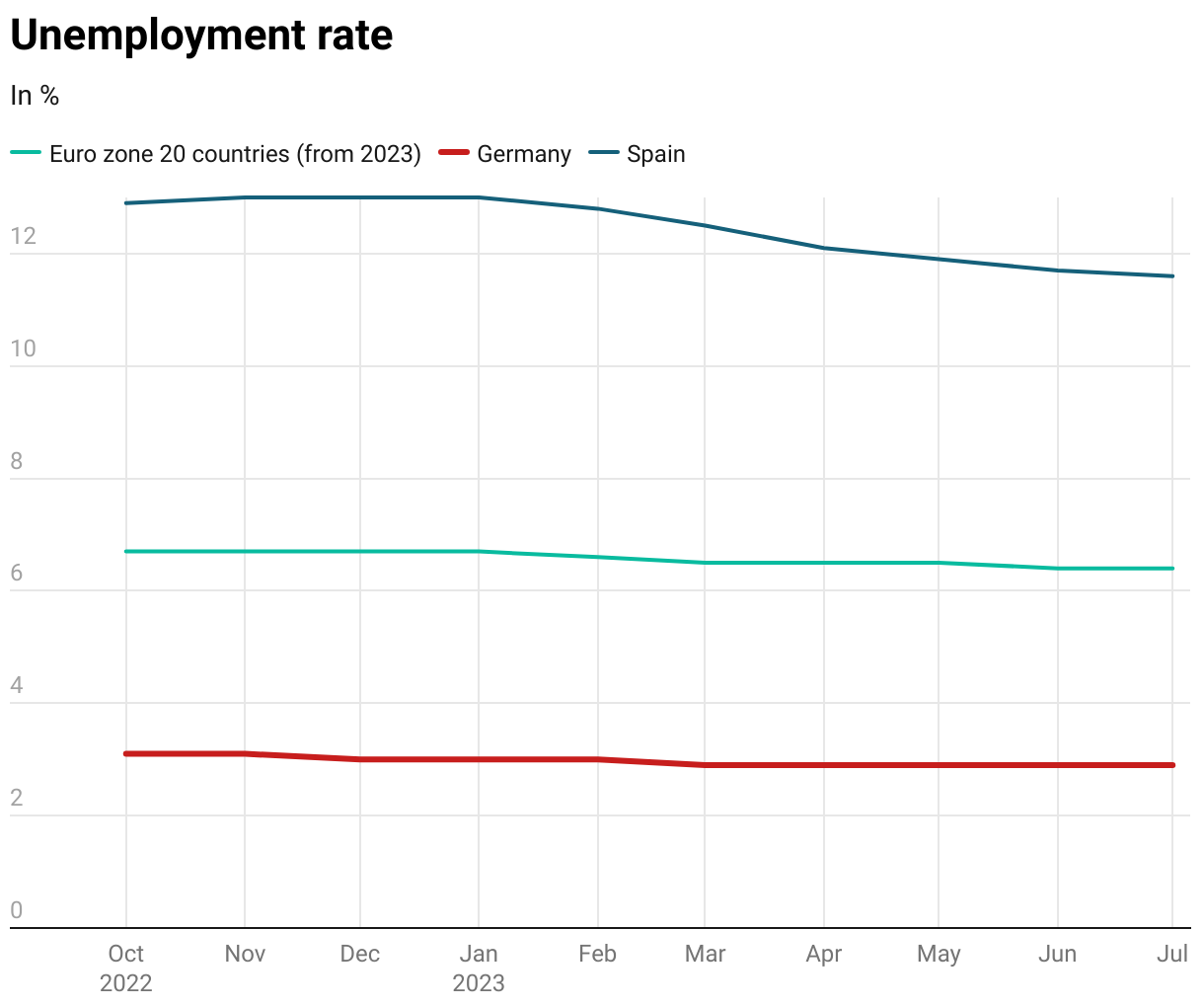

The German economy is now a far cry from the boom of the past decade: in the second quarter, its GDP remained stable (0.1%), after entering recession at the beginning of the year, and it has not experienced a real upturn since September 2022. In addition, inflation, the scourge of the past few months, is proving particularly resilient in Germany, which has been hardest hit by the energy crisis. High inflation and economic downturn have led to stagflation. That said, the nation does boast the lowest unemployment rate in the eurozone, and for economists such as Clemens Fuest, director of the Leibniz Institute for Economic Research (IFO), that renders the “sick man” label a slight exaggeration.

In terms of households, the signs ring true to the thrifty German mindset: while wages rose at their fastest pace ever in the second quarter (6.6%) — fueling fears of worsening inflation — household consumption remained stagnant, and consumer confidence indicators are sliding. The index compiled by the market research company GfK experienced a fresh setback this month, with a negative rate of 25.5 points on the eve of September. Nevertheless, Marcel Fratzscher, president of the economic research institute DIW Berlin, argues that as yet there are no signs of any second — round effects — when wage increases to mitigate the impact of inflation ultimately lead to further price rises — and he is confident that they can bolster consumption.

The change in the geopolitical order, disrupted by the invasion of Ukraine, has exposed the weaknesses of the German economic model. The German model, points out Wolfgang Münchau in one of his analyses for Eurointelligence, hinges on three ingredients: cost competitiveness, technological leadership in its industry and geopolitical stability, and ‘all of them are gone,’ he adds. On the one hand, the cut-off of Russian gas — which accounted for more than 50% of the gas consumed in Germany — has impacted the electro-intensive industry, forcing businesses like the chemical company Lanxess to restructure their business and close plants. In addition, with China in a slump, the overdependence of trade with the Asian giant has become evident: in July, according to the German statistics agency, exports to China — which represent 3% of Germany’s GDP — plunged by more than 6% on a year-on-year basis.

“The world around Germany has changed,” defends Münchau, “What has now emerged is an energy price crisis, new geopolitical divisions and technological shocks that pose existential questions about the future of the model.” In Fuest’s view, Germany will continue to depend on a substantial level of exports and imports, “but the industries that were successful in the last two decades, namely the chemical and automotive ones, will not perform the same role in the future.” Meanwhile, the business confidence indicator conducted by the institute over which Münchau presides posted its fourth negative month in August, and the perception of German businessmen stands at the levels of August 2020.

Berlin’s chances of reversing the situation in the short term remain slim, and the political landscape — a three-party coalition in government — does not make it any easier. At the end of 2021, social democrats, liberals and environmentalists signed the agreement that signaled the beginning of Olaf Scholz’s tenure as Germany’s chancellor after 16 years of a government under the leadership of Angela Merkel. Two central measures have been proposed by the coalition government: the establishment of a unitary energy price for the energy-intensive industry, championed by the Greens’ finance minister, Robert Habeck, and the approval of an ambitious tax package, put forward by the more liberal faction of the alliance, spearheaded by the finance minister, Christian Lindner. In the government’s first meeting after the summer break, differences between the liberals and environmentalists impeded the approval of the measure, which ended up being passed on Tuesday. It consists of a package of fiscal aid worth €32 billion over the next four years.

Structural problems

“The big challenge for the German economy is structural,” defends Fratzscher, at the DIW. The challenges are significant. Unemployment is at a record low, but it conceals something more worrying: according to Eurostat, in the second quarter the job vacancy rate was at 4.1%, one point above the eurozone average. This, coupled with a near non-existent unemployment, simply means that the labor force is unable to cover the jobs that the economy demands. And the explanation for this, as in many other developed economies, lies in the ageing population.

This is not a new problem. A decade ago, the Institute for Employment Research warned that between 2008 and 2050 the labor force will have diminished by 18 million people for demographic reasons alone. At the end of June, the German parliament approved a plan to lure skilled workers into the country.

Compounding a shrinking labor force and an over-reliance on exports come a series of hits that cut straight to the heart of the German economy, namely its industry. The main one is the energy transition, in which the government is investing billions of Euros, and which they estimate will take until at least 2027 to bring down energy prices for industry. For this reason, almost one third of companies are looking to invest outside Germany, according to the Chamber of Commerce and Industry’s Energy Transition barometer. Additionally, ING’s head of Germany and the eurozone, Carsten Brzeski, argues, the incentives contained in the US Inflation Reduction Act are attracting European companies, while “structurally weakening the industry.”

The mighty car industry has been particularly hard hit by all these factors, in addition to which, as analyst Patrick Artus points out in a report by the investment bank Natixis, there is competition from the thriving Chinese brands in the electric market. The Asian giant’s impact on Germany has a double edge. On the one hand, its weakness in recent months has been a burden on exports, while on the other hand, the momentum of brands such as BYD is threatening its industry. “China has become a more structural concern, as it no longer just purchases German products, but it has also become a competitor,” points out Brzeski.

Beyond an overdependence on exports, the challenge of the energy transition or an ageing population, there is an endemic ailment of the German economy, which has so far been masked by sound economic performance, and that is underinvestment. “The pandemic and the war in Ukraine have changed the world, but Germany has also failed to invest and implement new reforms,” says Brzeski, who identifies a need to “lead by example” during the austerity of the financial crisis as the cause. In a stable environment, the deficiencies in public investment — with their consequences for the country’s infrastructure — have gone unnoticed, but when there is an imbalance, an emergency arises.

According to Fratzscher, the industry “is lagging behind in comparison internationally” and needs to undergo a triple transformation: firstly, it has to accelerate its ecological transformation; secondly, it has “one of the worst digital infrastructures in Europe,” and many of its medium-sized companies have taken too long to digitize production, meaning that they have fallen behind in terms of productivity. And finally, it needs to reduce its dependence on China. In this process, and keeping in line with Brussels’ plans, the German government is seeking to attract large technology companies with a barrage of funds: a grant of €10 billion and Intel will invest a further €30 billion in the construction of two chip manufacturing plants in the city of Magdeburg. The Taiwanese TMSC will do the same in Dresden with a €5 billion government grant.

Economists point out that the transformation will require a combination of public and private investment, but they warn that this may clash with another endemic bugbear of the German system: excessive bureaucracy. “These investments are hampered by overly complex planning procedures, restrictive regulations and bureaucracy,” says Fuest at the IFO. “The German government needs to embrace transformation and foster its implementation rather than trying to consolidate the status quo,” explains Fratzscher: “This requires substantial public investment in infrastructure and education, as well as a simplification of regulation and bureaucracy.”

All the experts consulted agree that this process will require a sizeable financial commitment. In the opinion of ING’s Brzeski, the reversal of the country’s investment inactivity will only be possible if Germany changes its own fiscal rules — the constitutional debt restraint, suspended during the covid crisis. In addition, next year the European Union’s fiscal rules will return, which could serve as another hurdle for the country that for years played the role of the Old Continent’s fiscal police, allowing it to take the step that its economists are calling for. All of this has been coupled with the return of austerity rhetoric on the part of the government, and with the German far-right emerging as a force to be reckoned with. Curing the “sick man of Europe” will not be easy and it certainly will not be cheap.

Sign up for our weekly newsletter to get more English-language news coverage from EL PAÍS USA Edition