The United States is entering a tax crisis with skyrocketing deficits and debt

The federal government’s budget gap doubled in the 2023 fiscal year, and debt is on track to break the record set in World War II

In the United States, the numbers are not adding up. The country has entered a spiral of deficit and debt that originated in the 2007-2008 financial crisis, was aggravated by the Covid-19 pandemic and has not been resolved since then. In almost any other country, this lack of fiscal discipline would be unsustainable. And in the United States, some are beginning to fear that this is also the case for the country. The public deficit doubled last year due to the fall in tax revenue; debt held by the public is on track to surpass the World War II high, and long-term interest rates, due to a mix of factors, have hit 5%. With the aging of the population and the political deadlock in Congress, where Democrats and Republicans remain at loggerheads, the problem is only set to worsen.

The U.S. federal government’s fiscal year came to a close on September 30 and the budget execution data has just been published. It received $4.4 trillion in revenue collections and had $6.1 trillion of outlays, leaving a deficit of $1.7 trillion, the equivalent of 6.3% of gross domestic product (GDP). In 2022, the deficit was $1.37 trillion. These figures, however, are distorted. In 2022, the administration included as an expense a $379 billion plan to forgive student debt, but this plan never executed, as it was struck down by the Supreme Court in June. The $333 billion reversal was recorded this year as lower spending in 2023.

Taking this into account, the deficit more than doubled to $2 trillion (7.5% of GDP), a bar only surpassed during the two years of the pandemic. The main cause was the 9% drop in revenues. The U.S. Treasury said this shortfall was due to the fact that last year’s collection was particularly high thanks to the pandemic recovery and revenue from the capital gains tax. What has surprised analysts is that the deficit has soared in a period of growth and job creation, when the opposite is normally true.

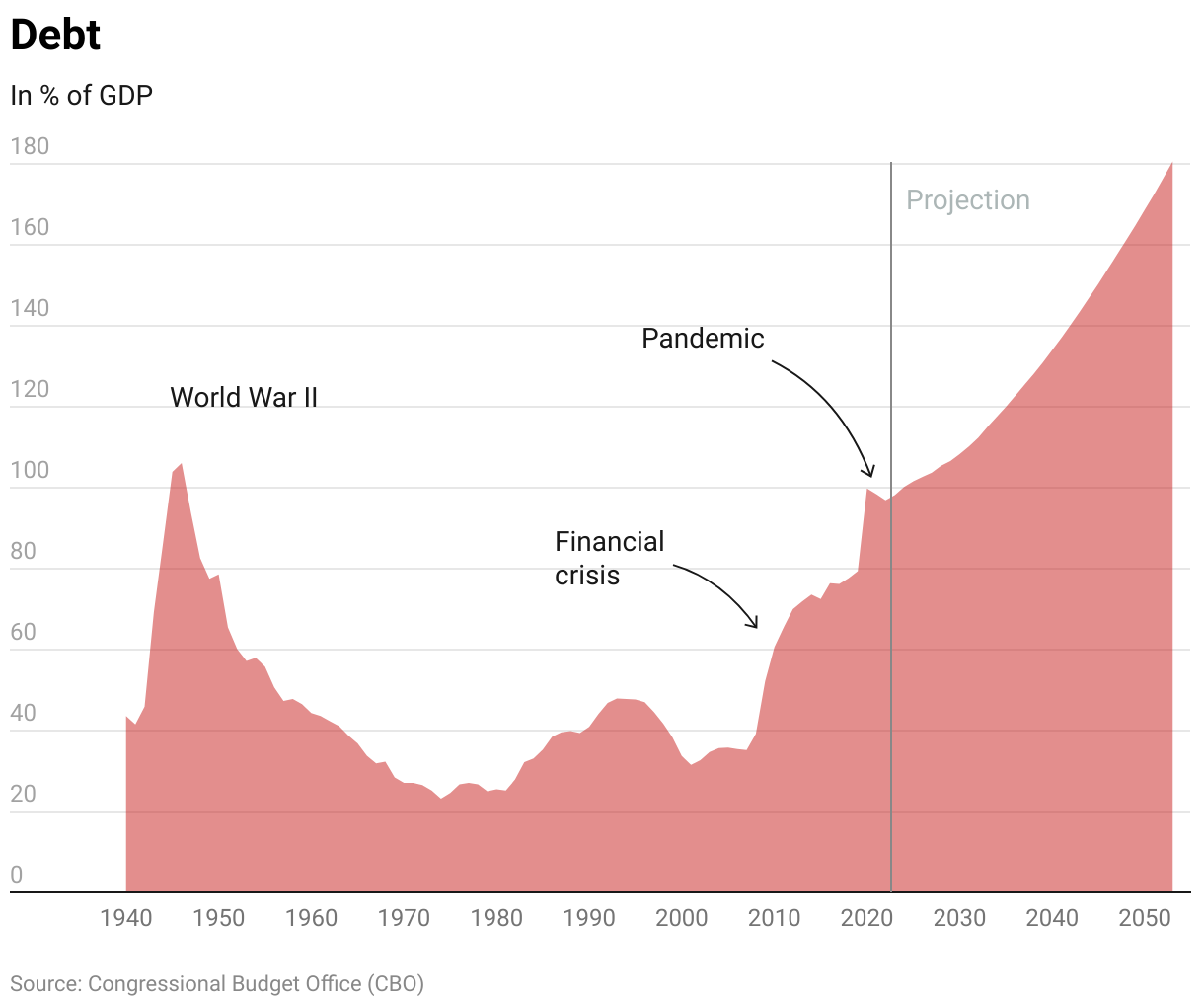

Gross public debt stood at 121% of GDP, but that figure is misleading as it includes $7 trillion in intragovernmental debt. The relevant data point is the amount of debt held by the public, which stood at 98%. Under this criterion, the U.S. public debt reached its historic peak at 106% of GDP in 1946 due to the effort of World War II. The strong growth of the following decades reduced it to 23% of GDP in 1974, before the oil crisis. Although it rose in the following decades, it still stood at a healthy 35% in 2007, before the financial crisis.

With the financial crisis, new spending items and tax cuts, it increased to 79.4% in 2019. The pandemic raised it to 100.6% of GDP due to extra spending and the drop in economic activity. Despite the subsequent recovery, the debt held by the public remained high. While it is by no means unsustainable for this figure to stand at 98% of GDP, the fiscal trajectory of the United States is unsustainable, even more so in an environment of high interest rates and persistent deficits.

Projections from the Congressional Budget Office, an independent body, suggest that the debt held by the public will surpass its all-time high in 2029, reaching 107% of GDP. The office predicts that it will rise to 115% in 2033; to 144%, in 2043, and to 181%, in 2053. “Such high and rising debt would slow economic growth, push up interest payments to foreign holders of U.S. debt, and pose significant risks to the fiscal and economic outlook; it could also cause lawmakers to feel more constrained in their policy choices,” it stated in its report.

“The unsustainable fiscal path in the U.S. is nothing new,” warned the Bank of America. “What is new are higher interest rates that are now priced to stay elevated for a longer period. Interest rate costs have a direct impact on how much the U.S. government needs to spend to finance its debt and contributes to the overall deficit.” It forecast that the deficit will hit $1.8 trillion in the new fiscal year, $1.9 trillion in 2025 and $2 billion in 2026. “Higher interest rates increase deficit spending and result in larger UST issuance, creating a spiral effect,” it added.

“A more significant fiscal adjustment will be required over the medium-term to put public debt on a decisively downward path,” noted the International Monetary Fund (IMF) in its latest report on the United States. “Achieving this adjustment will require a broad range of policies including both tax increases (even for those earning less than $400,000 per year) and addressing structural imbalances in social security and Medicare. The sooner this adjustment is put in place, the better.”

Political standoff

There is little room for maneuver to reduce the deficit without a sweeping overhaul. Budget laws only enable discretionary spending, which represents a decreasing portion. Not even the spending cuts demanded by Republicans would fix the problem. Regarding mandatory expenses, including pensions and public health care (Medicare), Democrats (and a good part of Republicans) consider them untouchable. On the other hand, Republicans (and some Democrats) flatly reject raising taxes . With a Republican-controlled Senate and a Democrat-contolled House of Representatives, the political standoff means any proposal to reduce the deficit is likely to be blocked.

The division in Congress could lead to a partial shutdown of the federal government if no agreement is reached after the short-term spending bill expires on November 17. Beyond the immediate disputes over spending, the first litmus test for fiscal policy will come, in principle, at the end of the 2025 fiscal year, when Donald Trump’s tax cuts — included in the 2017 Tax Cuts and Jobs Act (TCJA) — are set to expire.

“Of course, if Trump wins the next election, and assuming that the Republicans can regain full control of Congress, the likelihood of the TCJA being extended would increase substantially,” says Gilles Moëc, chief economist at the fund manager AXA Investment Managers. “This could be offset by decisive action on the spending side, but given the new demographics of Republicans, backing off on federal age-related health care and pay-as-you-go pensions may not be an easy sell,” he explains.

Moëc believes that the current president, Joe Biden, has “a comprehensive and internally coherent economic plan,” but that it is not designed to involve fiscal consolidation. “Where a Biden 2.0 administration would probably be more interested in addressing America’s fundamental fiscal problem than a Trump 2.0 administration is in its willingness to raise taxes,” he explains. But in order for Biden to raise taxes, the Democrats would need control of both the Senate and the House. The economist points out that the demands of the American people are “dissonant.” They want the spending on social security and healthcare as defended by the Democrats, but with the low taxes advocated by the Republicans, he says. Moëc points out that the market is going to begin to follow U.S. politics even more closely ahead of the 2025 presidential elections. “The market wants a little peace and tranquility. It is unlikely that it will get it from American politics in the near future,” he says.

Interest rates

There is little room for political action on taxes and spending. Likewise, interest rates depend on the level of public debt and market rates, which are not controlled by the government. The rise in debt rates, which makes it more expensive to refinance maturing securities, has sparked a debate about what has caused the spike. Initially, it was linked to the Federal Reserve’s tightening of monetary policy. But it has now reached a paradoxical point, where the market can both temper its expectations of future rate hikes by the Fed and demand higher long-term yields.

The debate is whether these high rates reflect the strength of the U.S. economy, as Treasury Secretary Janet Yellen argues, or whether the fiscal path is being penalized with a kind of risk premium, even though U.S. Treasury bonds are considered, by definition, a risk-free asset. “We suspect that an increasing number of investors are starting to look under the hood of the trajectory of the U.S. deficit,” says Moëc, who emphasizes the large amount of debt to be issued.

Tiffany Wilding, an economist at PIMCO, believes the bond selling that has driven up long-term rates “is largely driven by investor expectations of an increasingly strong U.S. economy” rather than concerns about more rate hikes. She explains: “We believe the sell-off is due to reduced recession expectations, which could ultimately lead to an increase in the supply of U.S. Treasury bonds,” which stands at $3.5 trillion. Wilding admits that it may seem “counterintuitive” because normally greater growth increases revenue and reduces the deficit. However, that is not currently happening, because in the absence of an imminent recession, central banks can reduce their bond holdings to a greater extent.

Garret Melson, portfolio strategist at fund manager Natixis, says the rate hikes “has left many investors scratching their head and looking for any justification for the move.” But rejects the “tidy narrative” that bond vigilantes and deficit spending are to blame.

“The current fiscal position of the U.S. is not problematic, but it’s no surprise that the path is unsustainable. The need to finance a widening fiscal deficit is not new news that investors suddenly discovered over the summer months,” he says. “The need to finance a widening fiscal deficit is not new news that investors suddenly discovered over the summer months.” Melson also argues that if the sustainability of the fiscal path were to blame, the dollar should have fallen, when the opposite has happened.

“Yes, larger deficits translate to greater Treasury issuance which in the absence of increasing demand would drive yields higher,” he admits. “That is certainly part of the story, but the move in rates appears to be far a confluence of events creating a buyers’ strike as opposed to any single smoking gun like deficit fears.”

Melson says possible explanations may include macroeconomic volatility, doubts about how growth and inflation will evolve, and uncertainties surrounding the Treasury’s issuance plans to finance the persistent deficit. “The marginal buyer of U.S. Treasuries is increasingly price sensitive. Pair a more price sensitive buyer base with a high volatility environment and you have the perfect conditions for a self-sustaining vicious cycle. High vol begets lower marginal demand which begets higher vol and around and around we go,” he explains.

Sign up for our weekly newsletter to get more English-language news coverage from EL PAÍS USA Edition