$12,000 a year to insure a home in Florida: Policies skyrocket due to the risk of hurricanes and floods

The forecast for this hurricane season is likely to lead to new hikes to prices, which have increased 100% since 2021. Many homeowners and insurers have left the state

When Mohammed Syed bought his 3,600-square-foot (335-meter) home in Pinecrest, Miami-Dade County, Florida, in 2017, he didn’t realize it was located in a flood zone. Until then, he had lived 10 minutes from his new residence and had never considered whether it was on land that was above or below the sea level. In a short time, he came face to face with reality. The mortgage required him to take out a flood insurance policy. “Now I have to pay $4,000 a year in insurance for that,” Syed laments. The problem is that he has to pay for two other policies: one to cover the risk of wind damage and a general one for the home, which raised his home insurance budget last year to $16,000. That amount is double what he paid when you bought the home in 2017, but less than what you will pay this year. This week he was notified that the general home insurance premium has risen from $6,791 to $8,198. “Insurance is so out of control that people are leaving,” he says.

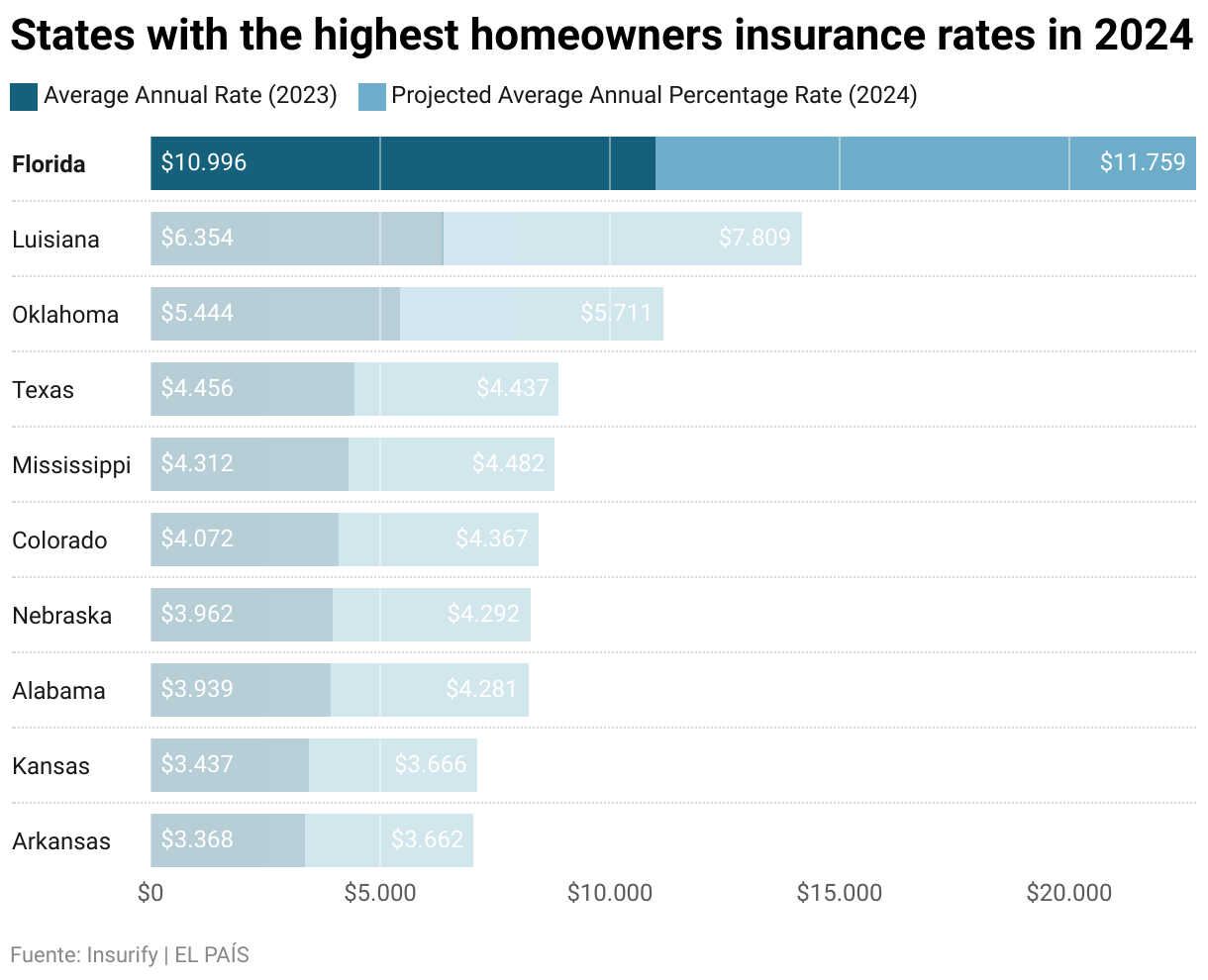

Real estate insurance prices have skyrocketed in Florida, soaring above the rest of the United States, and triggering a crisis that affects both homeowners and insurers. Average premiums reached $10,996 in 2023, according to Insurify data, compared to an average of $918 nationwide. This year, premiums are expected to rise by 7%, to $11,759. Since 2021, insurance has become more than 100% more expensive.

Since 2019, the crisis has led more than a dozen insurers to declare themselves bankrupt. Several to have voluntarily left Florida, and those still operating to refuse to insure many properties if they are located in high-risk areas.

“It is difficult to calculate the risk and insurers have years of losses. It has to do with the increase in population. More people are building homes in high-risk areas now, which means they’re more exposed once a disaster hits,” says Latisha Nixon-Jones, associate professor at Jacksonville University of Law.

Climate change

Florida is a peninsula surrounded by the Atlantic Ocean and the Gulf of Mexico, and more than half of the hurricanes that have made landfall in the United States have hit the state. Climate change and warming oceans have made the situation worse, and the likelihood of natural disasters has increased. This hurricane season, 23 severe tropical storms and 11 hurricanes — five of them of great intensity — are forecast. The state got its first glimpse of the season last week, when flooding was recorded in several areas of Miami due to heavy rains, which are expected to continue in the coming days.

Last year, Florida did not suffer major damage, only one — Hurricane Idalia — made landfall in the state. But in 2022, Hurricane Ian left a trail of destruction costing $60 billion, second only to Hurricane Katrina, which left more than $100 billion in damages.

A large portion of Florida is below sea level, meaning large areas of the state are exposed to flooding. Homeowners in those areas, like Syed, have to take out additional insurance to cover flooding and, in addition to the high price, they also have the problem of simply finding an insurer willing to cover them.

According to a Redfin survey conducted in February, 11.9% of respondents who plan to move out of Florida cited the cost of insurance as one of the reasons. In some cases, the cost of premium is more than the monthly mortgage payment. Additionally, more than a quarter of respondents said they fear their insurer will stop providing coverage.

Syed shares this concern: his policy has been canceled several times, most recently last year. “The inspection found some loose tiles and they canceled my policy. They could have been fixed, but they are very strict with damage to the roof,” he explains.

One of the reasons why insurers have fled Florida or stopped insuring certain clients is the high number of claims they are facing. “We are seeing more than 100,000 property claims a year in Florida, more than 80% of the total across the United States. It is obviously a disproportionate level and there was also a lot of fraud,” explains Mark Friedlander, director of the Insurance Information Institute.

New legislation

With the aim of addressing this problem, Florida legislators approved a new regulation in December 2022 that, among other measures, prevents third parties — not the owners — from filing lawsuits. “Unfortunately, some unscrupulous contractors were taking advantage of the situation and replacing roofs that did not need replacing or were not damaged by the storms,” says Friedlander.

The legal changes provide more security to companies. According to Friedlander, 10 insurers will not increase their prices this year and nine firms will enter the market. He recognizes, however, that it is still a volatile market and the fruits of the new legislation will take time to arrive.

According to Nixon-Jones, the market crisis is due not so much from fraud, but from unpredictability. “Insurers know that there can be disasters. However, it is difficult for them to calculate the risks and when they happen, they are greater than they thought, so they see their profits reduced,” she explains.

The problem for homeowners is that many cannot find an insurer willing to offer them a policy, which frequently happens in flood zones. In that case, they turn to Citizens, which is the insurer backed by public funds from the government of Florida, which covers properties that no private company wants to insure. To be covered, homeowners need to prove that there are no more options are available — a situation 1.2 million customers have so far shown. One of them is Syed, who turned to Citizens when one of his policies was canceled by his insurer.

Florida has tried to reduce the number of people insured by Citizens insures, but the opposite has happened. The state company receives 5,000 new policyholders every week. “Many clients still face high insurance bills, renewal bills, or problems finding coverage in the private market,” Friedlander admits.

The cost of insurance has become such a big problem that many homeowners have preferred to cancel their mortgage and finish paying off their house so as not to have to comply with the obligation to take out insurance. A luxury that, obviously, is only within the reach of a few.

Sign up for our weekly newsletter to get more English-language news coverage from EL PAÍS USA Edition